The market has yo-yo’d significantly over the past two years throughout the pandemic. Now that the country has largely recovered, it may feel like we’re “out of the woods”. Still, it feels as though the investment landscape is tough-to-predict – and that’s putting it lightly.

Historically, the “gold standard” 60/40 portfolio (60% stocks, 40% bonds) has treated investors well. Now, however, with stock market volatility and the value of bonds degrading, it feels as though there’s nowhere to hide. So, what are investors supposed to do?

This, among other reasons, is why you’ve heard the FPC Wealth team say that cash reserves that are specifically set aside to allow you to weather volatility in the short-term are critical.

Let’s talk about what you should do when the market fluctuates, and how you can keep your head above water when finances feel frustrating.

Look At Historical Data

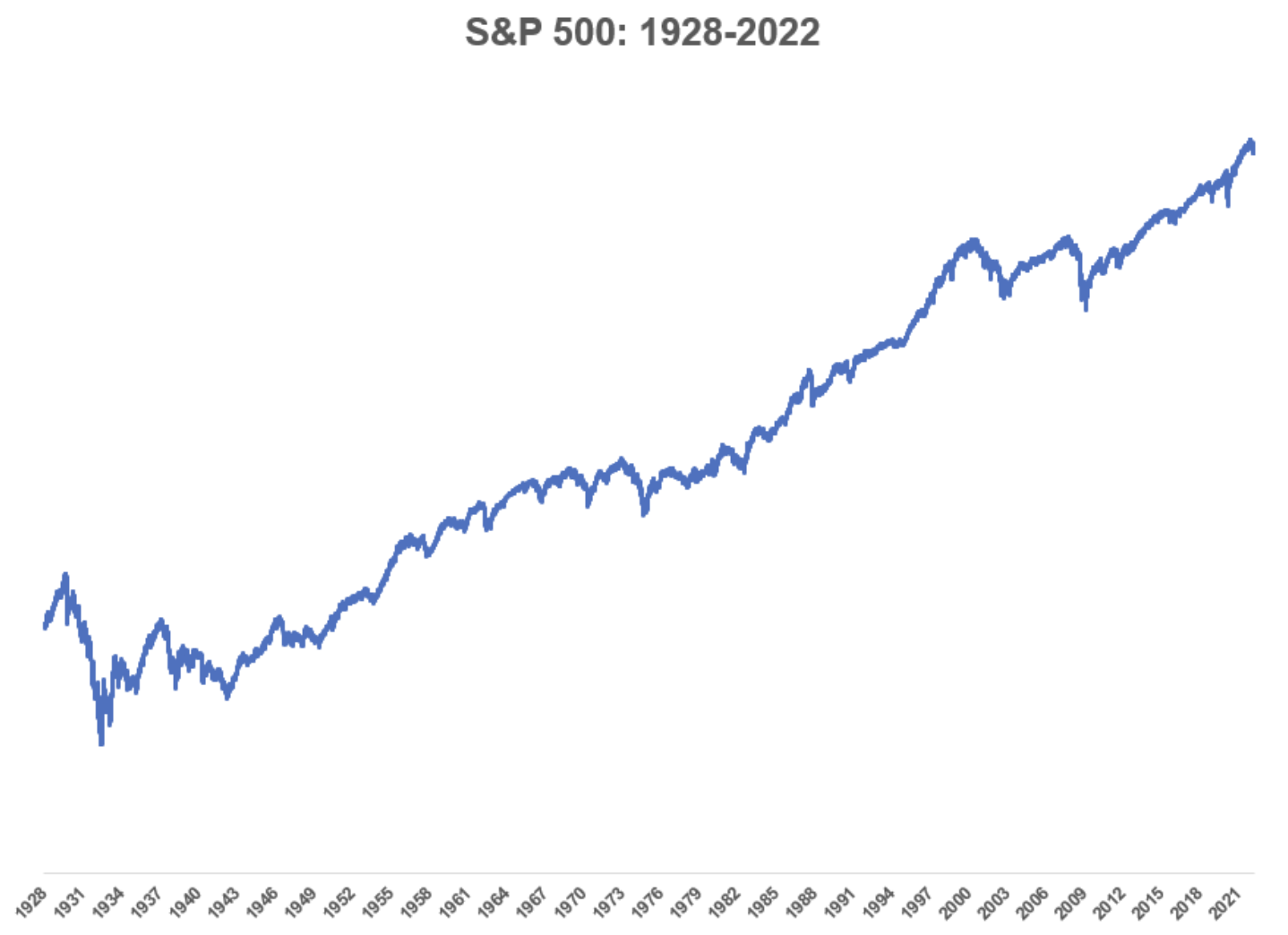

If you look at historical data, the market tends to trend upward over long periods of time. Of course, if you’re only looking quarter to quarter, or even year to year, it may not feel like this is the case.

Let’s look at the S&P 500 over the past 100 years as an example. As a note – the chart being used is the S&P 500, which was created in 1957, and then back filling the data using other indices of large market cap companies that existed prior.

Source: https://awealthofcommonsense.com/2022/05/why-does-the-stock-market-go-up-over-the-long-term/

Now, it’s not our expectation that investors are going to hold their investments over a 100-year period. Still, even when looking at shorter time intervals of 10-20 years, the S&P 500 still trends upward, even if there’s fluctuation from year to year.

It’s also important to keep in mind that the top 10 days of the market often make up the majority of portfolio growth over time. For example, in the past 20 years, the top 10 days of the market accounted for 75% of stock market returns for the period.

In other words, if you choose to go to cash when the market is down, you have the potential to miss a “top 10” day. Instead of making a rash decision due to (very valid) feelings of frustration, look at the historical data to reaffirm your strategy and refocus on playing the long game.

Remember Your Goals

Staying in alignment with your goals can help you to keep your head above water when it feels particularly tough to be an investor. Take an hour and sit down with your spouse or partner to review your goals, and where you currently stand.

This can look like a casual conversation about what you hope to achieve, or what your retirement timeline is. It may be a more in-depth analysis of your current spending, and setting some near-term goals (like boosting your cash reserves, completing a home project, or taking a vacation) that make it easier to track forward progress.

When it feels as though the economy is unpredictable, it can help to refocus on what’s most important to you. This takes you out of the cycle of fear and frustration, and pushes you to both have gratitude for where you are in your financial life right now, and to set your sights on goals that are relevant to you – not arbitrary market fluctuations.

Control What You Can

The truth is, we’ve had several years of stimulus checks, loan forgiveness, and heavy spending to get the country through the COVID-19 pandemic. Putting politics aside, these events in our recent history as a country are contributing to much of the economic volatility we’re seeing today. After all, there’s no free lunch! However, that’s not to say that living in the past and bemoaning decisions that were made two years ago at the height of a pandemic we knew very little about what is healthy for your emotional (or financial) state today.

We can’t control the past, and we often can’t control what happens on a government or societal level when it comes to the economy. Focusing on things that are outside of your zone of control is a recipe for unhappiness and financial frustration.

Instead, focus on what you can control. If you’re feeling anxious about your personal financial situation, now might be a good time to:

- Look to diversify your portfolio.

- Practice gratitude in your finances.

- Build your retirement strategy.

- Evaluate your spending habits.

- Boost your cash reserves.

Or take actionable steps to feel like you have a handle on your finances. These action items may not turn the tides in the market, but you’ll feel empowered that you’re doing the best you can with what you have.

Reach Out

Feeling frustrated about your finances?

Reaching out to your financial advisor during times like these can help you to vent with a neutral sounding board. Our team has been around the block, and is happy to offer insights on market fluctuations, inflation, and anything else that has you feeling concerned about your finances. We can help you to revisit your goals, check your progress, and make any suggestions for adjustments as needed.

Contact us today by clicking here – we’re here to help!