The economies of the world have come roaring back as the world slowly emerges from the pandemic lockdowns. With increasing vaccinations, massive fiscal stimulus, and extremely low interest rates, consumers around the world are opening their wallets.

Short-term growth in the global economies is tied to vaccination rates. According to the CDC (Center for Disease Control), there are almost 164 million Americans that have been fully vaccinated, or 49.4% of the U.S. population. The CDC recently announced that 70% of the adult U.S. population has received at least one dose of the Covid-19 vaccine.

The pandemic has created some new economic issues and solutions, and as such, we are reviewing a wider range of aspects of the global economies. We have listed some key bullet-points below to paint the picture of the current economic environment.

The U.S. & Global Economies:

- U.S. Leading Economic Index (LEI) increased 0.7% in June following a 1.2% increase in May and a 1.3% increase in April. The Coincident Economic Index (CEI) increased 0.4% in June following a 0.5% increase in May and a 0.1% increase in April. The Lagging Economic Index (LAG) was unchanged in June after a 0.6% increase in May and a 3.0% increase in April. The continuing increases in the economic indicators suggest further expansion and growth in the U.S. economy.

- Global GDP (Gross Domestic Product) is showing significant improvement as economies ease restrictions. The U.S. 2nd Quarter GDP came in at an annualized rate of 6.5%, which was less than expectations, but still noteworthy. Here are some future estimates of GDP growth from around the world:

| Country / Region | 2021 GDP | 2022 GDP | 2023 GDP |

| United States | 6.4% | 3.5% | 1.4% |

| Euro Area | 4.4% | 3.4% | 1.9% |

| China | 8.4% | 5.6% | 5.4% |

| Japan | 3.3% | 2.5% | 1.1% |

| India | 12.5% | 6.9% | 6.8% |

| Advanced Economies | 5.1% | 3.6% | 1.8% |

| Emerg & Dev Asia | 8.6% | 6.0% | 5.8% |

Source: IMF

- China’s growth continued to recover from the coronavirus pandemic. China had GDP growth of 7.9%, on a year-over-year basis, in the second quarter. The increase, while noteworthy, fell short of expectations of 8.1%.

- The Eurozone economies recovered nicely in the second quarter, turning in a 2.0% GDP growth rate from the prior quarter’s decline of -0.3%. The European economies appear to be making a strong recovery after they completed two quarters of negative GDP growth.

- Since the onset of the pandemic, the Fed has effectively reduced rates to zero (0.00% – 0.25%). Based on continuing statements from the Fed, there is little expectation of any near-term increases.

- Inflation in the U.S is currently at a 5.4% annualized rate for the month of June 2021 and is expected to remain in a range of 2-2.5% over the next few years. Global inflation rates are low with the advanced economies at 1.6% and are expected to remain below 2.0% over the next several years.

- Unemployment has declined steadily since the onset of the pandemic. The latest unemployment rate is now at 5.9% (as of June 2021). The Federal Reserve forecasts the unemployment rate in the US will slip below 4.0% by the end of 2021.

- In early 2020, oil prices (WTI – West Texas Intermediate) fell to a low of around $12 a barrel. Since then, oil prices have rebounded dramatically to a current price of ~$74 per barrel with expectations of further recovery as concerns of the pandemic subside.

- Consumer confidence (as measured by the Conference Board’s Consumer Confidence Index) remained steady in July but is now at its highest level since February 2020. As the consumer makes up nearly 70% of GDP growth, the increase in Consumer Confidence bodes well for continued resurgence as concerns over the pandemic abate in the U.S. economy.

- On the fiscal side, the Senate is moving toward passage of a $1 trillion bi-partisan bill. The House is working on a multi-trillion-dollar spending bill for the year ahead. The House is on recess and is not scheduled to return until September 20th. Notwithstanding, they are on a 24-hour call-back to vote on important issues.

- The U.S. deficit in 2020 totaled $3.13 trillion, its highest ever. Through June 2021 the year-to-date deficit is at $2.2 trillion and may surpass the previous year’s record-breaking deficit.

The U.S. & Global Equity and Bond Markets

Equities

- Large-Cap U.S. stocks did very well over the last twelve months as the economy reacted to the Fed’s low interest rates and Congress’s unprecedented stimulus packages. Large-cap stocks (as measured by the S&P 500 Index) did well with a 40.8% gain over the last twelve months (ending June 30, 2021).

- Historical and current consensus estimates for the S&P 500 earnings & price to earnings ratios (P/E):

- 2019 actual earnings $162.97: P/E 19.8 (S&P 500 year-end value at 3,230.78)

- 2020 actual earnings $139.76: P/E 26.9 (S&P 500 year-end value at 3,756.07)

- 2021 future earnings estimate $192.51: P/E 22.8 (S&P 500 value 4,395.26)

- 2022 future earnings estimate $214.17: P/E 20.5 (S&P 500 value 4,395.26)

- U.S. small cap stocks (Russell 2000) soared with a 62.0% return over the last twelve months (ending June 30, 2021).

- With the earnings season more than halfway over, 87% of companies in the S&P 500 have surpassed analysts’ expectations.

- European stocks (MSCI Europe) were up 35.1% over the last twelve months (ending June 30, 2021), as the European markets recovered from the initial stages of the Coronavirus pandemic.

- China (MSCI China Index) turned in positive results with a 27.5% gain (ending June 30, 2021). The results over the last year have been somewhat tempered by the deteriorating political relationship with the U.S.

- Technology (MSCI ACWI Information Technology) stocks turned in stellar performance with a 46.4% gain over the last year (ending June 30, 2021).

- Precious Metals (XAU – Gold & Silver Index) turned in a gain of 9.5% over the last twelve months (ending June 30, 2021).

- Energy stocks (XOI – Oil & Gas Index) performed well with a 45.1% return over the last year (ending June 30, 2021). This as a reflection of oil prices increasing as the economy recovers.

Bonds & Cash

- Short-term Interest rates remained low as the Fed continues to keep rates near-zero. Longer term rates have also fallen since the end of the first quarter. (See Treasury Interest Rates chart below).

- Longer-term bonds (ICE U.S. Treasury 20+year Bond) have gained 7.3% in the second quarter as interest rates fell. Notwithstanding, the index is down -7.91% YTD, and down -10.6% over the last twelve months (ending June 30, 2021).

Source: U.S. Department of the Treasury

FPC Team’s Insights & Perspective:

- As money market and bond rates are at very low levels, there is little room to make substantive returns in these asset classes. As such, equities continue to have the most opportunity of the broader asset categories.

- The global markets are awash in vast amounts of liquidity as the central banks have lowered interest rates, and governments continue to provide fiscal stimulus to their economies. Most importantly, vaccine rates are also moving higher, and consumers worldwide are working to satisfy their pent-up demand for goods and services which will lead to continued growth.

FPC’s Outlook

So, what is our view of the future? The economies have improved dramatically since the re-openings of businesses, and unemployment has dropped from their highs. There is a tremendous (one could say extraordinary) amount of both fiscal and monetary stimulus that has been injected into the economies of the world. The market(s) have seen a dramatic rise from the March 23, 2020 low. Since that low, the S&P 500 has jumped over 90%.

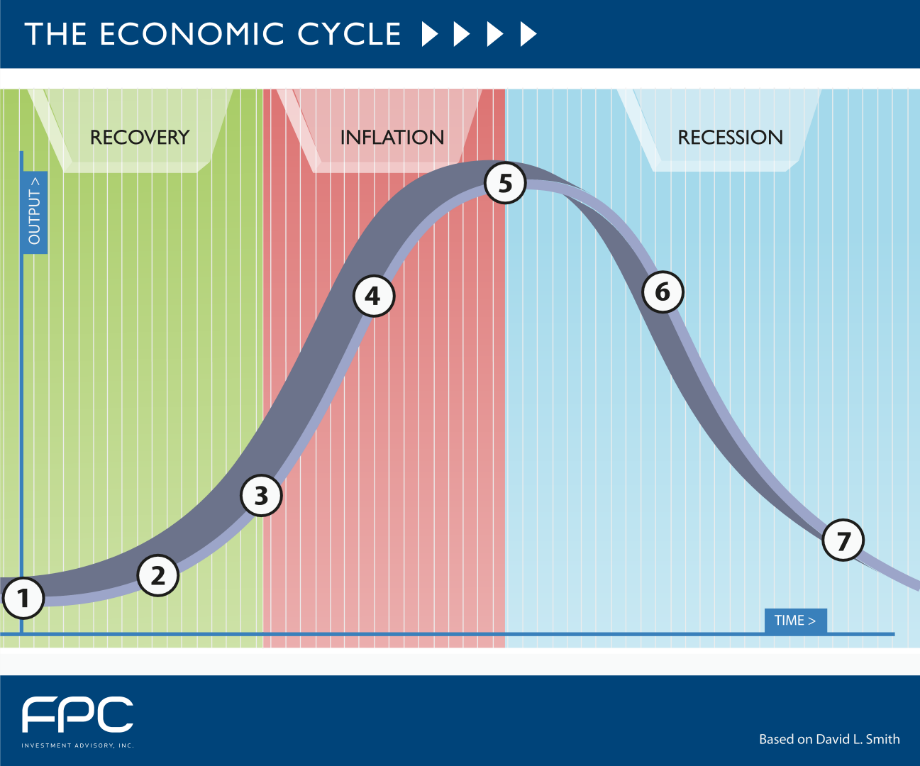

It is our belief that for the near-term future, the key indicator for the global economies will be the overall handling of the COVID-19 pandemic. As people resume their pre-pandemic lives, the economies of the world should see significant improvements. Notwithstanding, there are countries still suffering from the pandemic. The global economies appear to be in the early inflation phase (the U.S. is now between waypoint 3 and 4) which bodes well for the stock markets. See chart below:

The Economic Cycle

With historically low interest rates, expectations of additional fiscal stimulus, and a consumer with pent-up demand, equity markets likely have room to grow. We continue to maintain a minimum level of cash in the portfolios, since money market rates are virtually zero. The Fed will eventually be forced to raise rates to stave off inflation. Longer-duration bonds will decrease in value as interest rates move higher, so short-term bonds will continue to dominate our fixed income side of the portfolios.

We greatly appreciate the confidence you have shown in our services. Thank you for your business!

Sincerely,

Blair McCarthy & Bijan Golkar, CFP®