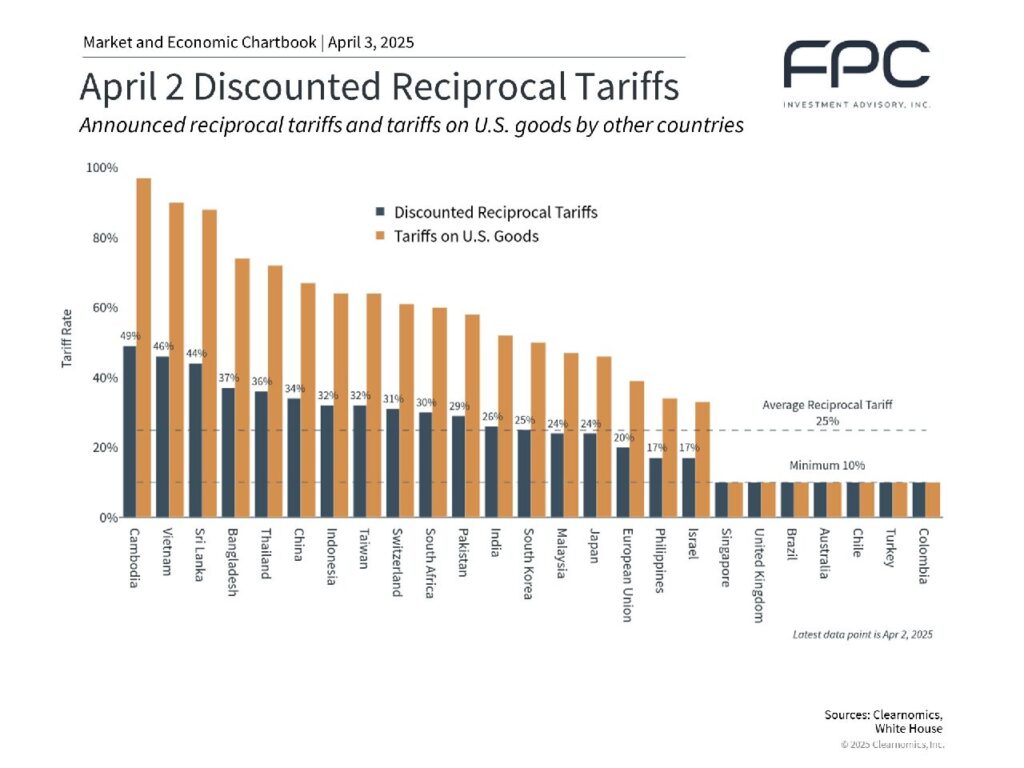

On April 2, President Trump announced new tariffs on nearly all major trading partners. These tariffs are “reciprocal” in that they correspond to tariffs each country imposes on U.S. goods and are on top of previously announced duties. The average tariff rate across countries is 25%, with rates for some as high as 49%. While the implementation of these tariffs was widely telegraphed by the White House, the level and scope are greater than many investors and economists expected. The immediate market reaction was negative, with the S&P 500 declining over 3% and the 10-year Treasury yield declining to around 4%.

The White House Has Announced Reciprocal Tariffs

There are many arguments for and against tariffs, and the topic can be politically charged. Regardless of how we each feel about these measures, we can acknowledge that these tariffs do represent a significant change in the global economic system.

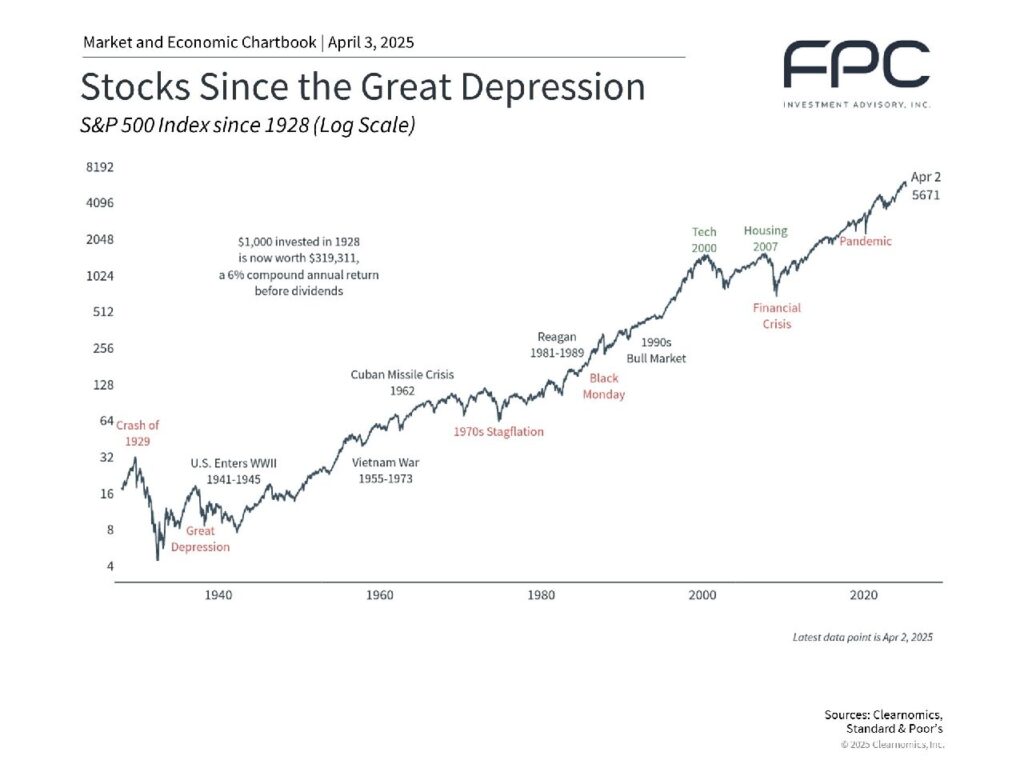

It’s important in times like these to remember that markets can be fragile in the short run but are resilient in the long run. Over the past century, markets have experienced significant global economic shifts including wars, recessions, bubbles, pandemics, political change, and technological revolutions.

In times of uncertainty, it can feel as if markets will never stabilize. Yet, history shows that markets can overcome even the most significant shocks, and often rebound when it’s least expected, as they did in early 2009 after the global financial crisis, in mid-2020 during the pandemic, in late 2022 after a technology-led bear market, and across countless other examples.

Having the fortitude and discipline to stay invested and stick to a personalized financial plan – or even to take advantage of more attractive valuations – is a key principle to long-term financial success.

Let’s cover some of the key facts. The newly-announced tariff measures have been set at a minimum 10% rate, with levels varying based on the U.S. trade deficit with each country. China, for instance, faces a reciprocal tariff rate of 34%, which is in addition to 20% tariffs previously announced. The European Union will be subject to 20% tariffs, while Canada and Mexico will not be immediately impacted by new reciprocal tariffs, and are instead subject to the previously-announced 25% tariffs related to illegal immigration and fentanyl. There is also an across-the-board 25% tariff on all imported automobiles, effective immediately.

The United States has a long history of tariffs, and in fact they were the primary source of federal revenue prior to the establishment of the federal income tax system in 1913. However, they fell out of favor after World War II as globalization took hold.

The administration’s arguments for tariffs are to raise revenues and ensure economic fairness, especially in the manufacturing sector – a policy it has dubbed “make America wealthy again.” President Trump’s long-stated goal of reducing the trade deficit and the view that trade is unfairly balanced were on display in his April 2 speech.

Arguments against tariffs are that they effectively tax consumers who ultimately pay higher prices for goods. This is particularly sensitive today due to the inflation that households have experienced over the past few years. Historically, it’s argued that periods of high tariffs may have worsened the Great Depression and slowed global economic growth.

Trade War Uncertainty is Fueling Market Volatility

Perhaps the most important perspective for long-term investors is that this shift in trade policy will be an ongoing process. The current round of tariffs truly began after the presidential inauguration, with the “America First Trade Policy” signed on January 20. The president’s trade position has been clear, even if there were questions about what policies would actually be enacted. These latest moves show that the administration is resolved to make significant changes, but even these could be negotiated with each country over time as they were during the first Trump administration.

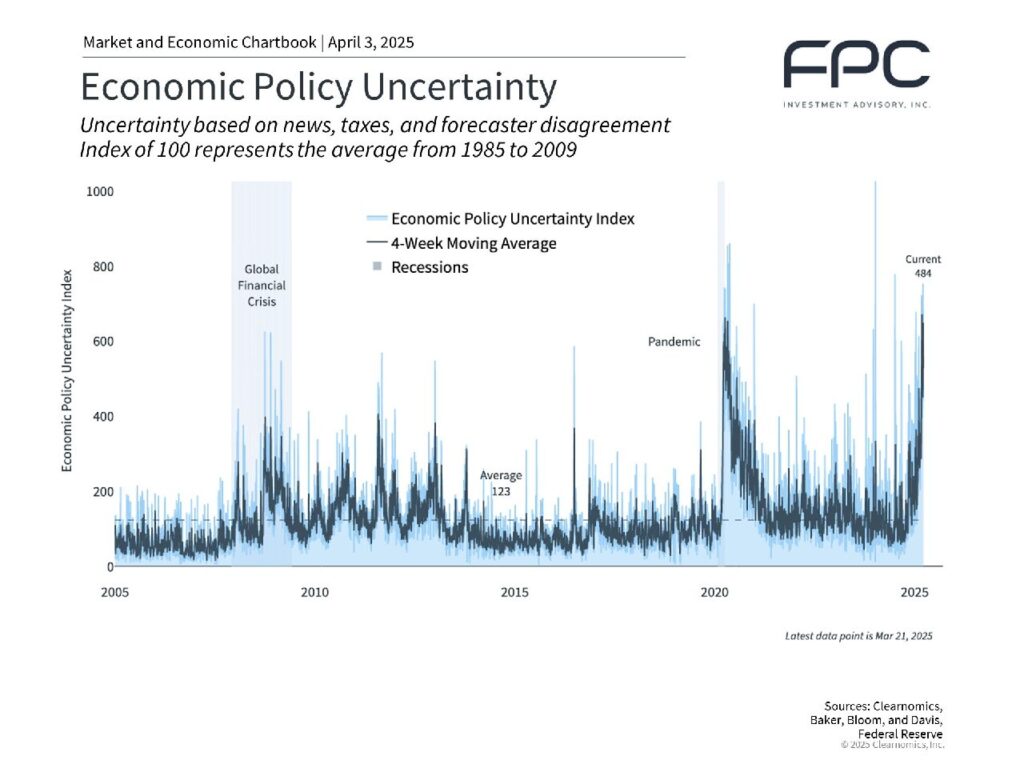

How does this affect markets and companies? It will take time to truly understand the impact, although some areas will be affected more than others. The general fear is that tariffs could shock the economy, potentially spurring inflation and slowing economic activity. As such, markets have already reacted negatively this year.

For example, while some domestic manufacturers might benefit from less foreign competition, markets tend to view trade barriers as negative for corporate profits, at least in the near term. Just as in the past, new trade policies force businesses to reconsider how they operate. They may adjust their sourcing strategies and can consider absorbing portions of the tariffs themselves.

In response to the 2018 tariffs, a portion of S&P 500 companies shifted their supply chains out of countries like China to reduce the impact from tariffs. These corporations relocated manufacturing facilities, found alternative suppliers, or adjusted their global production networks. While this can help companies navigate this latest round of tariffs, it takes time to adjust supply chains.

The S&P 500 sectors that are most directly impacted could be the ones with the greatest proportion of revenues coming from international sources. Nearly 30% of S&P 500 sales come from overseas, with information technology, materials, communication services, consumer staples and energy having the largest exposures according to Standard & Poor’s.

In addition to the impact on revenues, tariffs will likely affect company profit margins by raising costs for foreign-sourced components. Prior to the April 2 announcement, the estimate for 2025 S&P 500 earnings growth had fallen to 11.5% from 14.2% at the start of the year, according to FactSet. However, it’s important to note that this is occurring at a time when operating margins are historically high and productivity growth is rising. This could provide some cushion for profits.

One important fact is that a weaker dollar can be positive for both investors and companies as well. When it comes to asset allocation, international stocks have performed better this year, and a weaker dollar means that international assets are potentially more valuable in U.S. dollar terms. For companies, a weaker dollar can spur foreign sales since the cost of U.S. goods sold abroad becomes cheaper for foreign buyers.

Markets Rise Over Long Timeframes Despite Major Setbacks

Despite the immediate market reaction, it will take time for the true impact of these trade policy changes to play out. In recent years, investors have faced numerous market concerns including the pandemic, inflation, the possibility of a Fed policy error, recession fears, and more. Each of these challenges likely felt insurmountable at the time to some.

Yet, markets not only recovered, but rose to new levels over the following years and decades. While the past is no guarantee of the future, there is no reason to believe markets and the economy will not move past the current set of concerns.

Perhaps Warren Buffett said it best in 2008, during the middle of the global financial crisis: “In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.”

This is a helpful reminder that although market swoons can be unsettling, history shows that keeping a long-term perspective is the best way to stay on track to achieve your financial goals.