The start of 2026 delivered a constructive backdrop for investors, with both stocks and bonds extending the momentum that carried markets through the end of last year. This resilience may have seemed counterintuitive given recurring bouts of volatility driven by geopolitical tensions and shifting expectations about Federal Reserve policy. Headlines drove sharp but short-lived market moves, including the S&P 500’s worst single-day decline since last October. Even so, markets recovered quickly, and major indices reached new all-time highs within days. Healthy corporate earnings once again provided the fundamental support that helped steady portfolios.

For long-term investors, January offered an important reminder. Short-term market reactions to news are often unpredictable. Over time, fundamentals, discipline, and alignment with a long-term financial plan matter far more than any single headline.

Key Market and Economic Drivers in January

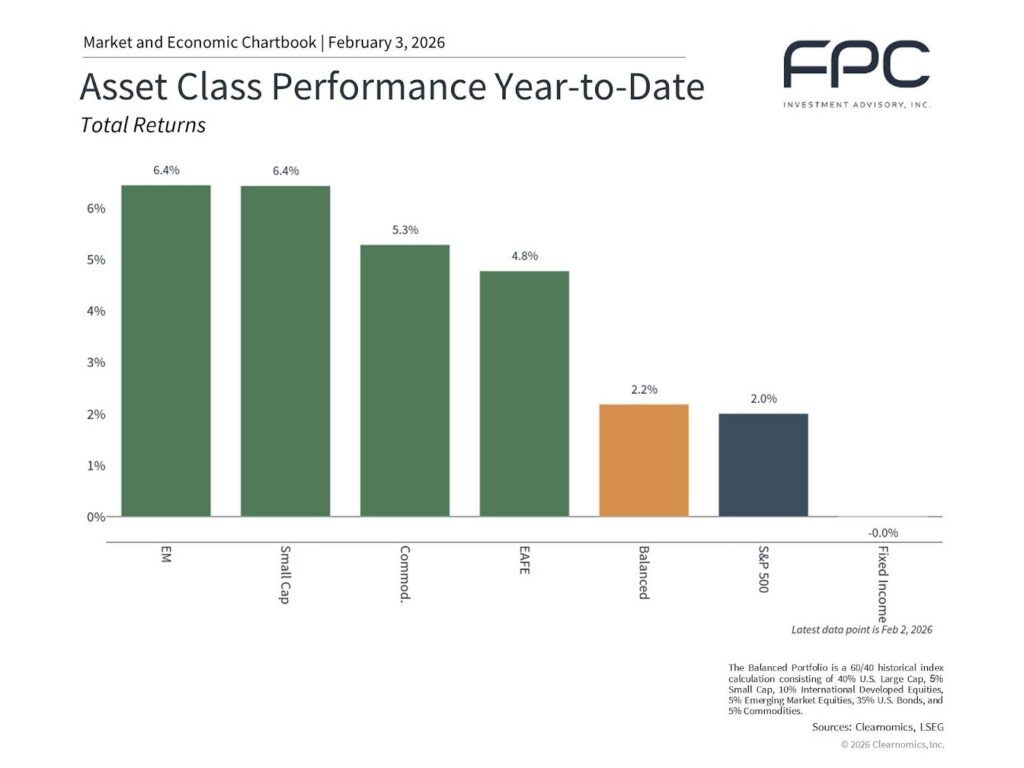

• The S&P 500 gained 1.4% in January and briefly crossed 7,000 on an intraday basis. The Nasdaq Composite rose 0.9%, while the Dow Jones Industrial Average gained 1.7%.

• The CBOE VIX volatility index ended the month at 17.44 after briefly rising above 20 amid geopolitical tensions.

• The Bloomberg U.S. Aggregate Bond Index advanced 0.1% as long-term interest rates moved higher. The 10-year Treasury yield finished the month at 4.24%, its highest level since last September.

• International developed markets rose 5.2% in U.S. dollar terms based on the MSCI EAFE Index. Emerging markets gained 8.8%.

• President Trump announced his intention to nominate Kevin Warsh as the next Federal Reserve Chair.

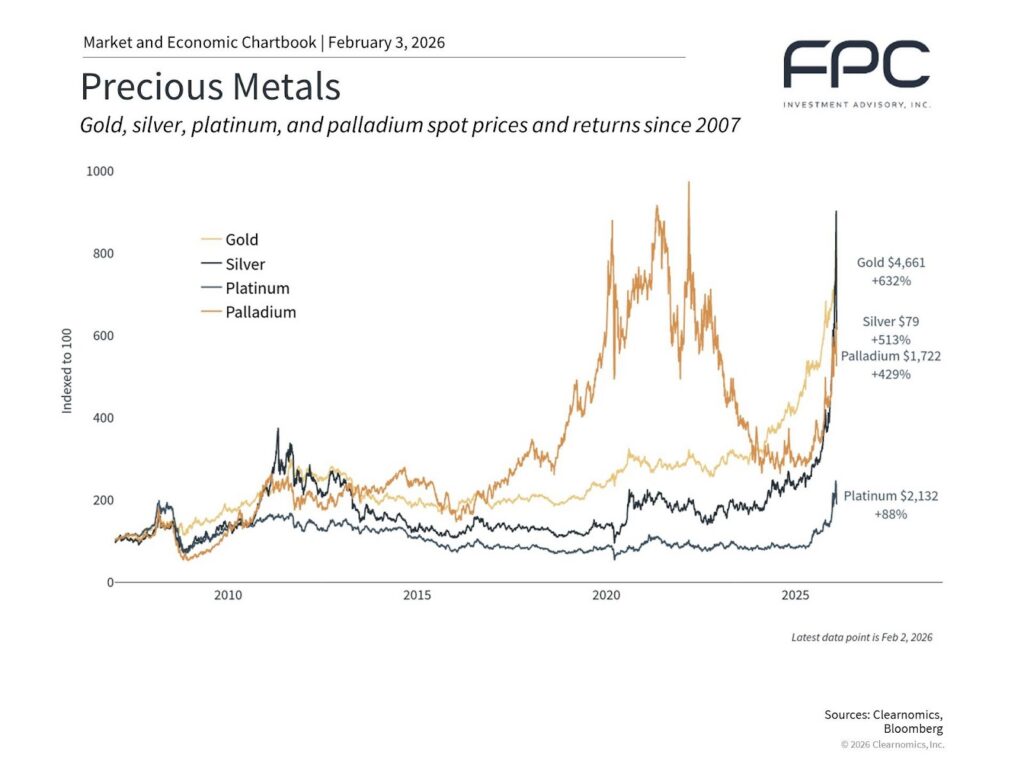

• Gold surged to a record close of $5,417 per ounce before declining sharply late in the month.

• The Federal Reserve held its policy rate at 3.50% to 3.75%.

• Consumer inflation remained above the Fed’s 2% target.

• Severe winter weather caused temporary energy price spikes.

Geopolitical tensions edged market volatility higher

Early in the month, a U.S. operation in Venezuela resulted in the capture of Nicolás Maduro. Investor focus quickly turned to energy markets. Venezuela holds the world’s largest proven oil reserves but produces less than 1% of global crude output. Geopolitical events most often influence markets through commodities, with oil remaining central to global economic activity.

Concerns escalated following U.S. statements regarding Greenland. Diplomatic tensions briefly intensified, contributing to heightened volatility. The situation de-escalated quickly after renewed dialogue, and markets rebounded as uncertainty faded.

Fed uncertainty drove swings in gold, silver, and the dollar

Precious metals rallied through most of January before reversing sharply late in the month. These moves reflected geopolitical risk, central bank demand, and questions around Federal Reserve independence.

The rally was often described as the “debasement trade,” reflecting concerns about deficits, accommodative policy, and dollar weakness. Expectations shifted following the announcement of Kevin Warsh as the next Federal Reserve chair nominee, leading to a sharp pullback in gold and silver.

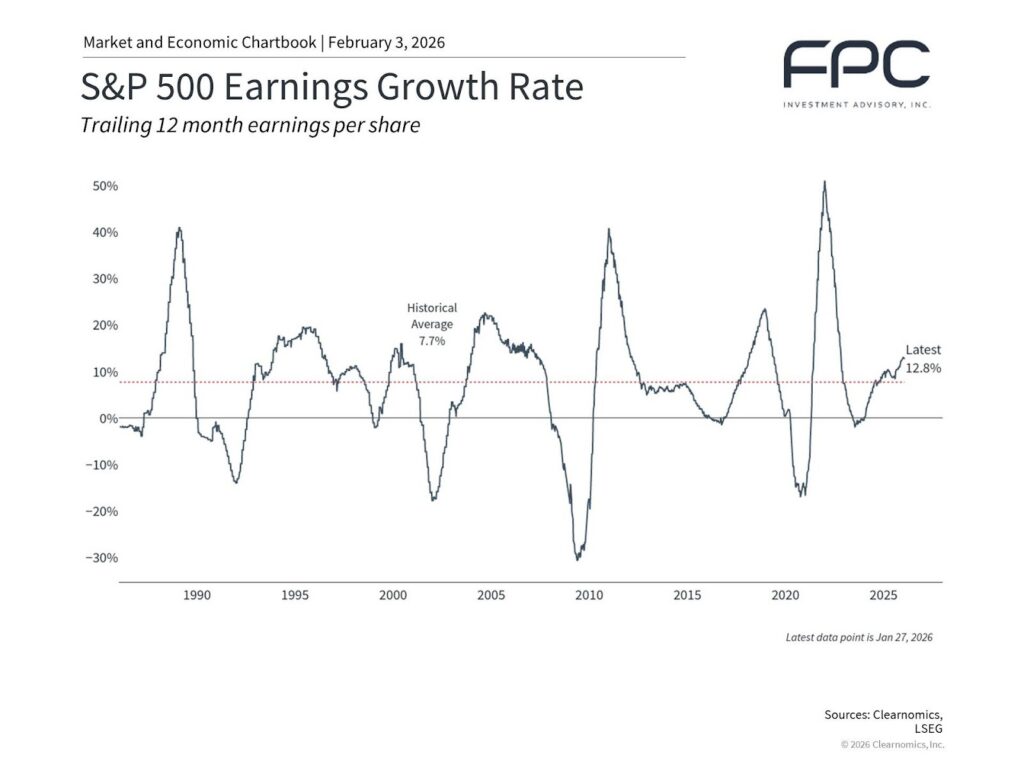

Corporate earnings remained resilient

Fourth-quarter earnings results continued to point to underlying economic strength. Approximately 75% of reporting companies exceeded expectations. Earnings growth remains broad-based beyond technology.

Severe weather disrupted activity, but not the outlook

Winter Storm Fern affected more than half of the U.S. population. While disruptions were significant, history suggests such events tend to delay, rather than destroy, economic activity.

Bottom line

January was marked by volatility driven by geopolitical tensions, Federal Reserve policy uncertainty, and extreme weather. Markets remained resilient, supported by strong earnings. For long-term investors, maintaining a disciplined, diversified investment strategy aligned with financial goals remains the most effective approach.